The Dark Side of Prediction Markets: Insider Trading and Who Really Earns

Why Trust Web3Bet

Our team of experts has independently reviewed and evaluated all the products and services featured on this page to ensure you receive accurate and reliable information

Insider trading in traditional finance involves buying and selling securities using material non-public information without fulfilling one’s fiduciary obligations, such as a company director selling their shares because they know the company faces imminent losses or a crash. This practice in the US, for instance, is regulated by the SEC, and similar regulations exist in the EU and other parts of the world.

However, prediction markets are loosely regulated, making it easy to indulge in insider-type activity. One may then ask how stock markets and prediction markets are alike. First, it must be noted that, like with other types of exchanges, you have contracts and the order book, and prices arise from matching buyers and sellers. It is precisely the nature of prediction markets that makes them susceptible to insider trading. Individuals who are privy to information seek every means to monetize it, and prediction markets provide an avenue to do so. In this article, we will explore some of the most interesting “insider trading” cases on Polymarket.

What “Insider Trading” Means on Prediction Markets

Insider trading in traditional finance involves buying and selling securities using material non-public information without fulfilling one’s fiduciary obligations, such as a company’s director selling their shares because of knowledge that they face an imminent crash or losses. This practice in the US, for instance, is regulated by the SEC, and similar regulations exist in the EU and other parts of the world.

However, prediction markets are loosely regulated, making it easy to indulge in insider-type activity. One may then ask how stock markets and prediction markets are alike. First, it must be noted that, like with other types of exchanges, you have contracts and the order book, and prices arise from matching buyers and sellers. It is precisely this nature of prediction markets that makes them susceptible to insider trading practices. Individuals who are privy to information seek every means to monetize it, and prediction markets provide an avenue to do so. In this article, we will explore some of the most notable real-world examples.

Case #1: The 2024 US Election Markets

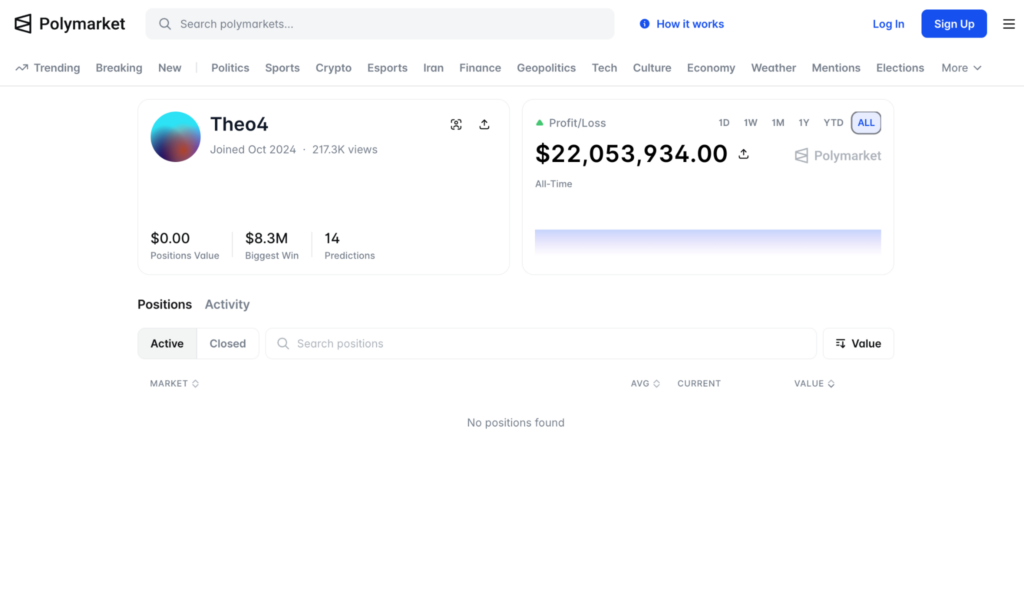

This is, perhaps, the most unusual trader on Polymarket. The account is no longer active; he is most likely using a different one now.

Let’s start with perhaps the most famous example. The 2024 U.S. presidential election was an unprecedented event in prediction market history, in both trading volume and media coverage. An anonymous “whale,” a major market participant, appeared on the Polymarket platform; initially known as the “French Trader,” he was later billed in the press as the “Trump Whale” (or “Theo”).

On the back of around 11 accounts, he placed tens of millions of dollars in bets on Donald Trump’s victory by trading in numerous separate contracts. Chainalysis put its time-weighted net profit at $80-85 million (one of the most lucrative bets of all time in crypto markets), a conclusion echoed by several media reports.

Here are some of the especially noteworthy aspects of the case: He employed multiple accounts, as well as an additional “layering” strategy of placing bets, in order to avoid skewing the order book with a single large bet and to conceal the true size of his position.

With press reports in the Wall Street Journal, Financial Times, and Business Insider indicating he ordered up his own private opinion polls in YouGov, he focused on otherwise sensitive corporate research on the Blue Wall (Pennsylvania, Michigan, and Wisconsin) swing states, making the biases of publicly released poll numbers more evident.

The powers-that-be, including the French gambling regulator, were extremely alarmed not only by the enormous scale of this activity, but also by how closely these monitors resembled classic insider trading.

In real time, it was impossible to separate an “all-knowing” user using independent studies from a government agent or campaign insider with substantial nonpublic information. In the market, however, the outcome was equivalent: a large amount of capital makes the market price converge toward its “rational” levels, regardless of whether the most-informed gambler was a campaign insider or not.

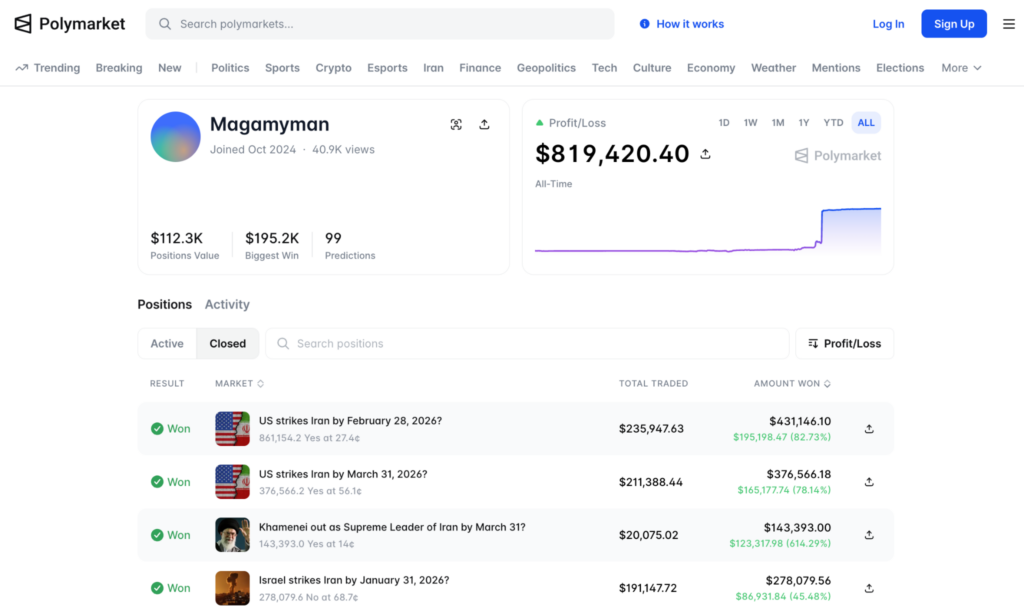

Case #2: Polymarket Trader “Magamyman” made $553,000 on Iran Strike

The Magamyman profile also became inactive a month ago. However, many positions remain open.

Sometimes the market “guesses” events too accurately. 71 minutes before the news of a US strike on Iran, a Polymarket user named Magamyman opened a large position when the probability of the event was estimated at only 17%, turning approximately $87,000 into $515,000 overnight. This sparked a media scandal in the US.

The timing and size of the bet on the attack outraged members of Congress: senators openly discussed banning or severely restricting Polymarket, and the White House was forced to explain how people with access to sensitive military information could monetize it through an on-chain market rather than store it in closed channels.

An analysis of the on-chain activity surrounding this case revealed a complex structure of fund movements: transactions were conducted through cross-chain bridges, linked wallets, and addresses associated with crypto infrastructure in offshore jurisdictions. Overall, this looks more like a well-thought-out scheme than a random guess.

Such stories highlight a simple fact: the blockchain may appear anonymous at first glance, but all transactions remain forever. Over time, as data accumulates and connections between addresses are analyzed, a clear picture increasingly emerges from this noise.

Case #3: Half a million for USA-Iran escalation

The goooofy profile also stopped being active. Why so, eh?

Sometimes the market “guesses” war too accurately. Ahead of the recent escalation between Israel and Iran, Polymarket trader @goooofy reportedly made over $500,000 by taking a highly concentrated position on the outcome.

Essentially, this is yet another “Pentagon analyst” who, using better-than-average access to information, bet around $82,000 on a favorable, familiar scenario—and was proven right.

Cases like @goooofy’s are a reminder: blockchain only appears anonymous at first glance. Every transaction remains forever. As on-chain data accumulates and behavioral patterns are analyzed, what previously looked like a collection of random addresses and “lucky guesses” increasingly resembles a coherent picture of how insiders systematically outpace the news.

The Regulatory Outlook

The SEC and CFTC are aware that the prediction markets have an insider trading problem. Whether they will be successful at constraining this insider trading is a different matter. On regulated sites, such as Kalshi, the CFTC has the authority to investigate suspicious trading for cause and to bring enforcement actions. Trouble is, the information traders in the political prediction market use is not illegal information to possess or trade upon. The securities law rules for insider trading on non-securities markets are much weaker.

For decentralized markets, there is no enforcement. There is no one to subpoena, no centrally tracked trading data available for regulators to pull, and no one to shame. The end result: regulated prediction markets will develop more advanced surveillance tools to identify suspicious trading with enforcement actions as a deterrent, while decentralized prediction markets will thus continue to operate in a regulatory black hole. Retail traders will remain vulnerable.

What will happen to insider trading?

The main takeaway: insiders on Polymarket always have, always will, and always do. Individuals with access to secret government, military, or corporate intelligence routinely cash in on their knowledge through prediction markets (e.g., Polymarket-like platforms).

For most of us mere mortals, it’s impossible to spot them amid the chaos of the market; you just observe that the probabilities have been priced for some event as if a massive position has been snapped up. But it is important to understand that US regulations against insider trading did not arise simply because “it’s unfair that someone else knows more,” but because insider trading is a breach of trust, a betrayal of the confidence reposed in someone.

One example: You are informed about an upcoming M&A deal involving your employer and buy up stock options. The company trusted you with confidential information, and you abused that trust, risking harm to the employer if they were to lose due to your upcoming actions. That’s a breach of trust, and a big red flashing warning sign for the legal hit squad.

Another example: You are on a plane, and two CEOs are arguing about the same M&A deal you just were told about. Two minutes later, you buy options. You learned the information unintentionally and had no obligation to anyone other than yourself, so they had no reason to expect loyalty or to be betrayed.

Consequently, this probably wouldn’t be trademarked as classic insider trading. (This isn’t legal advice.) Now, to prediction markets (Polymarket, Kalshi, etc.): while they may have clear internal bans on insider trading, that doesn’t mean the US federal securities laws against insider trading don’t apply to them. This remains a grey legal area: it’s far from certain whether, and if so to what extent, the securities laws apply to “prediction markets.”

Likewise, the special forces Operative who placed a wager on Maduro’s position will most likely be indicted not under classic insider trading laws but rather under the theft and unauthorized use of classified US government information laws and for breach of NDAs. From a meta standpoint, the “insider trading” here is that he used classified information to make a prediction about a specific task.

Do you think prediction markets should be banned? Some argue, as Thomas Peterffy, for example, that such markets are critical for enabling precise predictions about the likelihood of future events; after all, when insiders take part in a market, odds are heavily refined and very frequently accurate.

On the other hand, detailed knowledge, even about the tiniest minute and insignificant events, can be a very big problem: if you’re running a clandestine covert black ops operation, the last thing you want is some guys on the other side to get a friendly warning hours in advance just by looking at Polymarket.